International traffic for Indian carriers notably surpasses pre-Covid levels

Elevated aviation turbine fuel (ATF) prices and INR depreciation are likely to pose a serious threat to the recovery process for domestic carriers

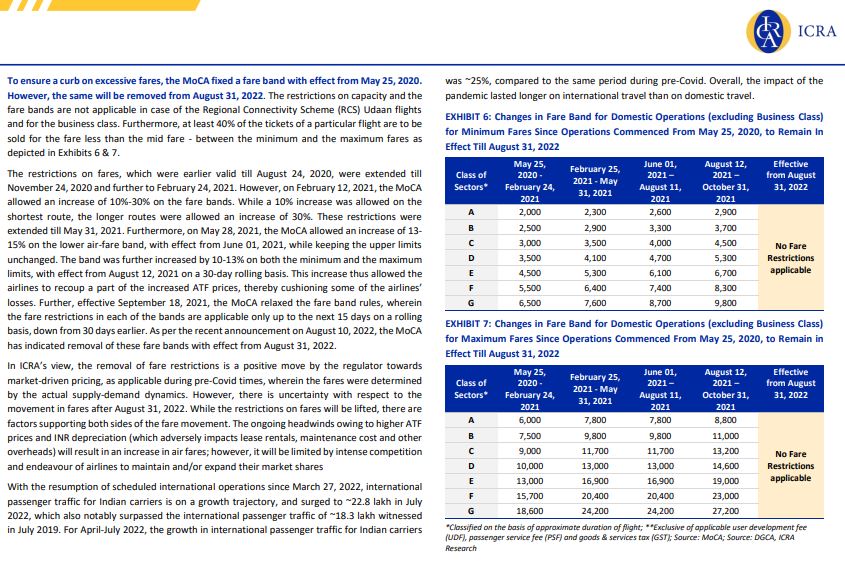

Removal of fare restrictions from August 31, 2022 to enable domestic airlines to price as per market supply-demand dynamics, thereby enabling passing on the escalated input costs by way of fare hikes wherever possible

With the return to normalcy in the business environment, domestic passenger traffic grew by 94% on a YoY basis to ~9.7 million in July 2022 (5.0 million in July 2021) and was only ~18% lower compared to ~11.9 million in July 2019 (pre-Covid level). On a sequential basis, however, it was ~7% lower compared to ~10.5 million in June 2022, given some impact of the cyclicality in passenger travel, mainly arising from the lean period during monsoon coupled with impact on leisure travel due to hardening of air travel fares. The airlines’ capacity deployment for July 2022 was ~65% higher than in July 2021 (78,614 departures in July 2022 against 47,692 departures in July 2021). On a sequential basis, the number of departures in July 2022 were lower by around 5% compared to June 2022.

Commenting further, Suprio Banerjee, Vice President & Sector Head, ICRA said, “For July 2022, the average daily departures were at ~2,536, notably higher than the average daily departures of ~1,538 in July 2021, and slightly lower compared to ~2,771 in June 2022. The average number of passengers per flight during July 2022 was 124, largely in line with the average of 126 passengers per flight in June 2022 and higher than the average of 105 passengers per flight in July 2019. ICRA believes that the domestic air traffic yields^ have moved up in the range of 25-30% over pre-Covid levels on domestic routes. The industry earnings in FY2023 will continue to reel under pressure owing to the elevated ATF prices, coupled with the depreciation of the INR against the US$, given that around 35-50% of the airlines’ operating expenses are denominated in US$. Although removal of fare restrictions from August 31, 2022 will partially enable domestic carriers to pass on the escalated cost by way of fare hikes, the possibility of such sharp fare hikes is limited, given the intense competition.”

With the resumption of scheduled international air operations since March 27, 2022 and reversion to bilaterally agreed capacity entitlements, the international passenger traffic for Indian carriers is on a growth trajectory and surged to ~2.3 million in July 2022, notably surpassing the international passenger traffic of ~1.8 million in July 2019 (pre-Covid level) by ~25%.

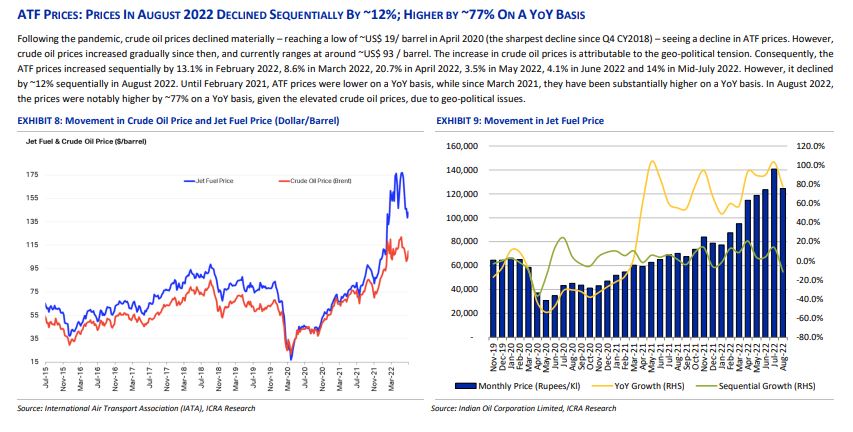

An area of concern remains the ATF prices, which surged by ~77% on a YoY basis in August 2022, given the elevated crude oil prices, due to geo-political issues arising from the Russian invasion of Ukraine. Although, ATF prices declined by ~12% sequentially in August 2022, they continue to remain at elevated levels, which is likely to hinder the recovery in the earnings for the industry in FY2023.

On an aggregate basis, a return to normalcy will lead to recovery in passenger load factors, which in turn will aid revenues; however, elevated ATF prices and INR depreciation will continue to weigh on the earnings of Indian carriers in FY2023. This apart, the expected launch of Jet Airways and the entry of a low-cost carrier, Akasa Air, is expected to intensify the competition for Indian carriers.