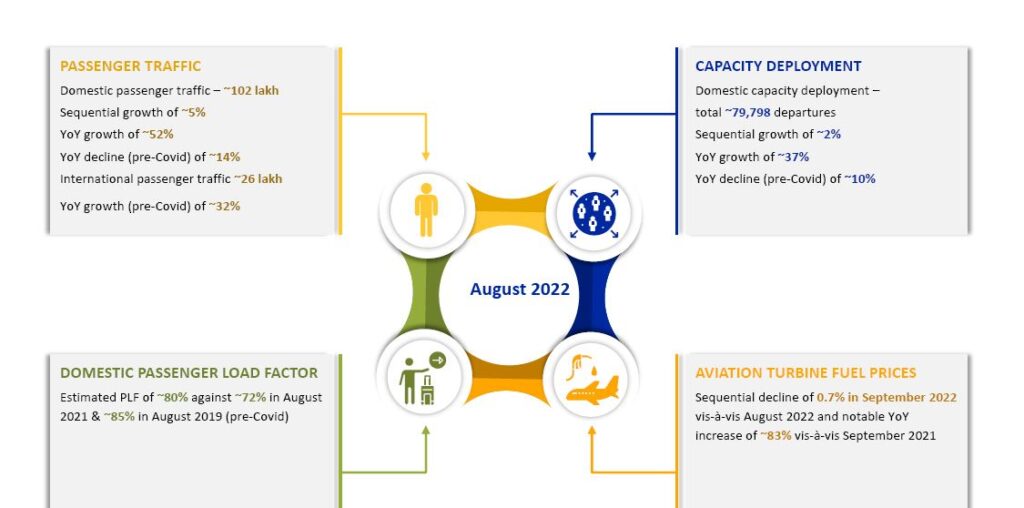

The domestic aviation industry continues to witness recovery, with domestic passenger traffic for August 2022 estimated at ~102 lakh, ~5% higher compared to ~97 lakh in July 2022 and ~52% higher in comparison to the domestic passenger traffic in August 2021, although it fell short by ~14%, compared to pre-Covid levels i.e. August 2019. For 5M FY2023 (April-August 2022), domestic passenger traffic is estimated at ~524 lakh, a YoY growth of ~131%, and lower by ~11% compared to April-August 2019.

The airlines’ capacity deployment in August 2022 was ~37% higher than August 2021. However, it was lower by ~10% than the pre-Covid levels. It is estimated that the domestic aviation industry operated at a passenger load factor (PLF) of ~80% in August 2022, against ~72% in August 2021 and ~85% in August 2019. The international passenger traffic for Indian carriers in August 2022 strongly surpassed the pre-Covid level of ~19.8 lakh by ~32%.

A steady rise in prices of aviation turbine fuel (ATF) and a general inflationary environment continue to dampen the industry earnings, with ATF prices in September 2022 higher by ~83% on a YoY basis. However, the same declined by 0.7% sequentially. While airlines have been increasing yields, in ICRA`s view the same has not been adequate to offset the impact of the rising ATF prices.

A quick recovery in domestic passenger traffic is expected in FY2023, aided by normalcy in operations and waning pandemic. However, the earnings recovery for domestic airlines will be slow-paced due to elevated ATF prices in addition to the rupee depreciation against the US$ amid a heightened competitive environment.